Morningstar DBRS Confirms Bank of Hawaii Corporation’s Long-Term Issuer Rating at ‘A’; Trend Stable

The following is a press release distributed by DBRS Morningstar.

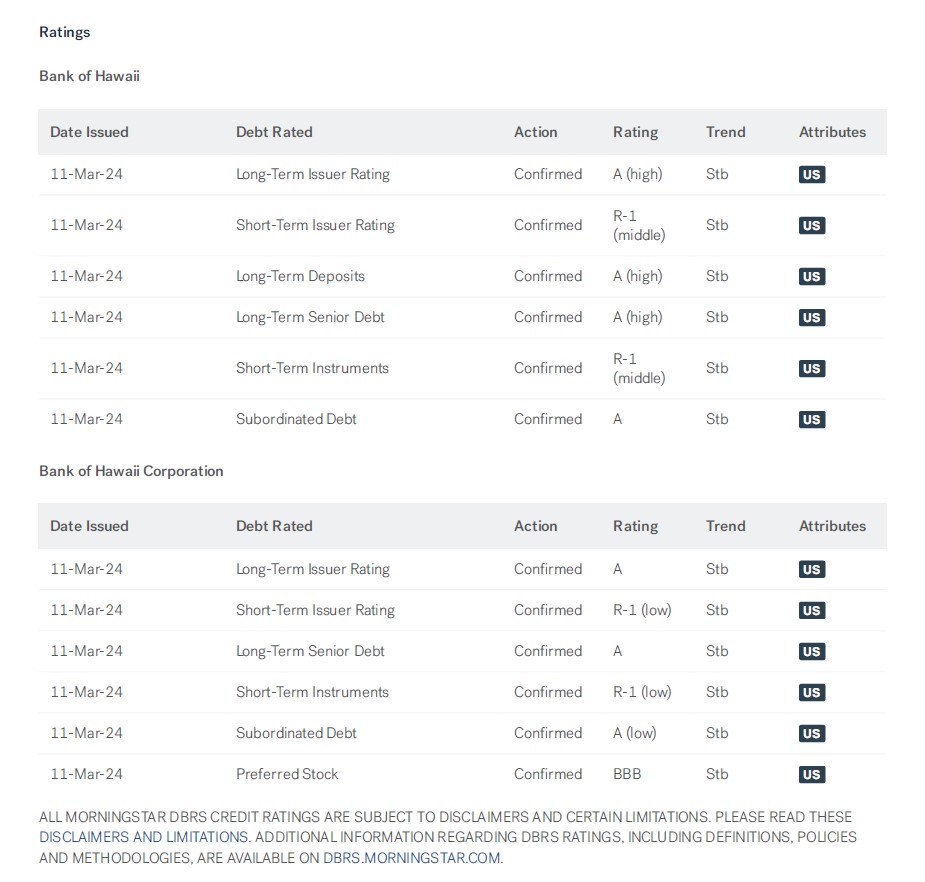

March 11th, 2024

DBRS, Inc. (Morningstar DBRS) confirmed the credit ratings of Bank of Hawaii Corporation (BOH or the Company), including the Company’s Long-Term Issuer Rating of ‘A’. At the same time, Morningstar DBRS confirmed the credit ratings of its primary banking subsidiary, Bank of Hawaii (the Bank). The trend for all credit ratings is Stable. The Intrinsic Assessment (IA) for the Bank is A (high), while its Support Assessment remains SA1. The Company’s Support Assessment is SA3 and its Long-Term Issuer Rating is positioned one notch below the Bank’s IA.

KEY CREDIT RATING CONSIDERATIONS

The credit ratings confirmation and Stable trend reflect BOH’s strong banking franchise that is underpinned by a deeply entrenched presence within the Hawaiian islands. In addition, the Company consistently generates strong financial results, while sustaining sound balance sheet fundamentals. The credit ratings also consider BOH’s dependence on the Hawaiian economy and its high level of real estate exposure, substantially all of which is located within Hawaii, where real estate values have been quite resilient during recent economic downturns and are supported by a limited supply. Additionally, we also considered unrealized losses in the held to maturity securities portfolio and their potential impact on earnings and capital if in the unlikely scenario that these losses were realized.

CREDIT RATING DRIVERS

Over the longer term, the credit ratings would be upgraded if the Company can grow its fee-based businesses to enhance revenue diversification, while maintaining strong credit metrics and capital levels. Conversely, the credit ratings would be downgraded if there is substantial asset quality deterioration that results in sustained weaker earnings. A deterioration in funding stability, especially as a result of a material loss in deposit market share, would also result in a credit ratings downgrade.

CREDIT RATING RATIONALE

Franchise Combined Building Block (BB) Assessment: Good / Moderate

BOH benefits from having a strong brand and relatively limited amount of competition within the Hawaiian Islands. The Company operates the most branches in Hawaii and holds about a third of the total deposit market share. In addition, the Company is the top residential mortgage provider in the state.

Earnings Combined Building Block (BB) Assessment: Strong / Good

We view BOH’s earnings power as strong, having generated a double-digit return on equity (ROE) for 21 consecutive years, including in 2023. The Company reported $171 million of net income in 2023, which was down 24% from 2022, reflecting lower net interest income, higher expenses and a higher provision for credit losses. Still, returns remained sound including a ROACE of 13.89% for 2023. BOH’s loan portfolio is about 60% fixed rate loans, which limits the asset sensitivity of the Company’s balance sheet. Moreover, a large, albeit high quality, securities portfolio that is lower yielding given the rapid interest rate increases from the Fed to combat inflation will also be a headwind if higher rates persist. These concerns are partially mitigated by BOH’s large, stable, and low cost deposit base.

Risk Combined Building Block (BB) Assessment: Strong / Good

Consistently strong asset quality and conservative underwriting remain hallmarks of the Company. Asset quality metrics remained pristine and improved in some categories in 2023, with a net charge-off ratio of just six basis points for 2023 and NPAs of eight basis points at YE23. We note that 79% of the loan portfolio is secured with real estate (both residential and commercial), with a weighted average loan to value of 54%, providing a substantial buffer if real estate values were to weaken. Additionally, CRE office accounts for just 3% of total loans.

Funding and Liquidity Combined Building Block (BB) Assessment: Very Strong / Strong

BOH’s funding and liquidity is underpinned by a substantial low-cost, core deposit base, which easily funds the loan portfolio (66% loan-to-deposit ratio at YE23, unchanged from YE22), as well as a high-quality investment securities portfolio. Relative to 2022, deposits increased 2%, reflecting long-enduring commercial and consumer banking relationships, where the Company provides the main transactional accounts for households and businesses. In addition, the Company has $10.2 billion in readily available liquidity which exceeds the $8.9 billion in uninsured and uncollateralized deposits. The investment securities portfolio was $7.4 billion at December 31, 2023, a decrease of 10.3% from December 31, 2022. The investment portfolio remains largely comprised of securities issued by U.S. government agencies and U.S. government-sponsored enterprises. While higher interest rates has caused unrealized losses on the securities portfolio of about $1.03 billion, the Company continues to reduce investment securities to increase liquidity and decrease market risk.

Capitalization Combined Building Block (BB) Assessment: Strong / Good

Capital metrics remain sound, with a CET1 ratio of 11.33% at YE23. BOH’s well-capitalized CET1 ratio requirement is 6.50%, meaning that it has about 483 basis points in capital cushion to its CET1 capital requirement. The Company has also showed improvement in its TCE to TA ratio which ended the year at 5.07% up 38 basis points from 4.69% at YE22. The improvement represents higher capital levels as well as a reduction in investment securities and lower unrealized losses.

Further details on the Scorecard Indicators and Building Block Assessments can be found at https://dbrs.morningstar.com/research/429184.

ENVIRONMENTAL, SOCIAL, AND GOVERNANCE CONSIDERATIONS

There were no Environmental/Social/Governance factor(s) that had a significant or relevant effect on the credit analysis.

A description of how Morningstar DBRS considers ESG factors within the Morningstar DBRS analytical framework can be found in the Morningstar DBRS Criteria: Approach to Environmental, Social, and Governance Risk Factors in Credit Ratings at https://dbrs.morningstar.com/research/427030/morningstar-dbrs-criteria-approach-to-environmental-social-and-governance-risk-factors-in-credit-ratings (January 23, 2024).

Notes:

All figures are in U.S. dollars unless otherwise noted.

Morningstar DBRS applied the following principal methodology: Global Methodology for Rating Banks and Banking Organizations (June 22, 2023): https://www.dbrsmorningstar.com/research/415978/global-methodology-for-rating-banks-and-banking-organisations.

In addition Morningstar DBRS uses the DBRS Morningstar Criteria: Approach to Environmental, Social, and Governance Risk Factors in Credit Ratings https://dbrs.morningstar.com/research/427030/morningstar-dbrs-criteria-approach-to-environmental-social-and-governance-risk-factors-in-credit-ratings (January 23, 2024) in its consideration of ESG factors.

The credit rating methodologies used in the analysis of this transaction can be found at: https://dbrs.morningstar.com/about/methodologies.

The primary sources of information used for this credit rating include Morningstar, Inc. and company documents. Morningstar DBRS considers the information available to it for the purposes of providing this credit rating was of satisfactory quality.

The credit rating was initiated at the request of the rated entity.

The rated entity or its related entities did participate in the credit rating process for this credit rating action.

Morningstar DBRS had access to the accounts, management, and other relevant internal documents of the rated entity or its related entities in connection with this credit rating action.

This is a solicited credit rating.

The conditions that lead to the assignment of a Negative or Positive trend are generally resolved within a 12-month period. Morningstar DBRS’ outlooks and credit ratings are under regular surveillance.

For more information on this credit or on this industry, visit dbrs.morningstar.com.

DBRS, Inc.

140 Broadway, 43rd Floor

New York, NY 10005 USA

Tel. +1 212 806-3277

Contacts

John Mackerey

Senior Vice President, Sector Lead - North American Financial Institution Ratings

+(1) 212 806 3236

john.mackerey@morningstar.com

Michael Driscoll

Managing Director, Head of NA FIG

+1 212 806 3243

michael.driscoll@morningstar.com

You're about to exit BOH.com

Links to other sites are provided as a service to you by Bank of Hawaii. These other sites are neither owned nor maintained by Bank of Hawaii. Bank of Hawaii shall not be responsible for the content and/or accuracy of any information contained in these other sites or for the personal or credit card information you provide to these sites.