Tax Credits vs. Tax Deductions: Making the Most of Your Tax Benefits

Reading time: 5 Minutes

March 25th, 2022

Few people look forward to filing taxes unless they're anticipating a big refund. But taxes don't have to be intimidating. Learning about your options for filing taxes on your own and how tax brackets work can go a long way towards making tax season less, well, taxing. And if you want to reduce your tax bill (or increase your refund), it helps to have a basic understanding of tax deductions and tax credits.

What is a Tax Deduction?

A tax deduction reduces how much taxes you owe by lowering your taxable income. How much of a reduction depends on your tax bracket. For example, if you're in the 22% tax bracket, a $100 tax deduction reduces your tax bill by roughly $22.

Types of tax deductions

There are three main types of deductions that may help lower your taxable income: standard, itemized, and above-the-line deductions. Let's take a look at each.

Standard deduction

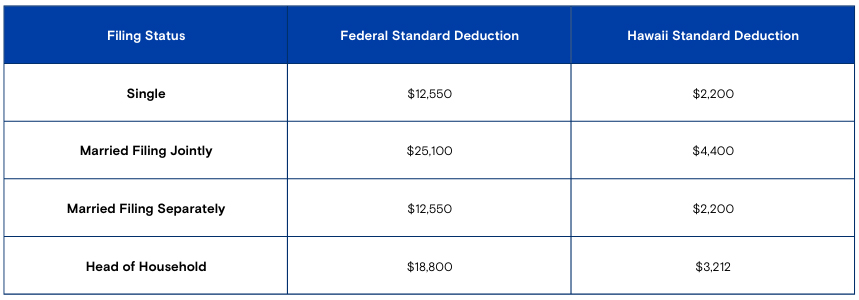

A standard deduction is a flat dollar, no questions asked reduction from your taxable income. The amount you qualify for depends on your filing status.

For the 2021 tax year (tax returns filed in 2022), the standard deductions are:

For example, if you are a single Hawaii taxpayer with a $50,000 salary, you can use the standard deduction of $12,550 to reduce your federal taxable income to $37,450 and state taxable income to $47,800.

Itemized deductions

Itemized deductions are expenses you incur during the year that can be subtracted from your taxable income. In order to take these deductions, the IRS requires you to provide evidence (like receipts, canceled checks, or copies of bank statements) for any expense you plan to use for a deduction. Some of these expenses can include:

- Medical expenses. You can deduct out-of-pocket medical expenses that exceed 7.5% of your adjusted gross income (Line 11 of Form 1040). You can find a comprehensive list of deductible medical expenses in IRS Publication 502.

- State and local taxes. You can claim your Hawaii state income taxes and property taxes on your federal taxes. Your total deduction for all these taxes is capped at $10,000.

- Home mortgage interest. You can deduct interest paid on up to $750,000 of home mortgage debt (or $1,000,000 of debt for mortgages taken out before December 16, 2017).

- Gifts to charity. You can deduct gifts of cash or property donated to a qualified charity.

- For gifts of property, certain limitation rules may apply. This year, for cash donations, there is no limitation. Visit the IRS charitable page to learn more.

- The IRS has a Tax Exempt Organization Search Tool to find out if your charitable donation is tax deductible.

Because the IRS caps the deductions for home mortgage interest and property taxes, for residents of states like Hawaii, where home prices and combined state and local property taxes can easily exceed the caps, claiming the standard deduction may be more beneficial than itemizing.

Above-the-line tax deductions

Above-the-line deductions, also known as adjustments to income are useful because you can claim them in addition to the standard deduction or itemized deductions. Subject to certain restrictions, in general, deductions can be made for the following:

- Expenses for K-12 teachers

- Contributions to a health savings account (HSA)

- Contributions to an IRA or self-employed retirement account

- Health insurance premiums for self-employed people

- Student loan interest

- Moving expenses for members of the Armed Forces

What is a Tax Credit?

Tax credits are a dollar-for-dollar reduction in the amount of tax you owe. Let's say you owe $1,000 in taxes, but can claim a $750 tax credit. Using the credit, you would only have to pay $250 in taxes.

Types of Tax Credits

There are two types of tax credits: refundable and nonrefundable.

Refundable tax credits

Refundable tax credits provide a refund, even if it's more than what you owe in taxes.

For example, say you owe $500 in taxes, but you qualify for a refundable credit of $1,000. In this case, you would receive a $500 refund.

Common refundable tax credits:

- Earned income tax credit (EITC): Gives low- to moderate-income taxpayers a refundable federal credit ranging from $1,502 to $6,728, depending on how many children they have. Hawaii also has a non-refundable EITC worth 20% of the federal credit.

- Child tax credit: Worth $3,600 for qualifying children under age 6 and $3,000 for qualifying children ages 6-17. The maximum credit is available to taxpayers with a modified adjusted gross income (AGI) of:

- $75,000 or less for singles

- $112,500 or less for heads of household

- $150,000 or less for married couples filing a joint return and qualified widows and widowers.

Nonrefundable tax credits

Nonrefundable tax credits reduce some or all of what you owe, but doesn't exceed that amount (does not provide a refund).

For example, say you owe $500 in taxes and qualify for a $1,000 nonrefundable credit. You would receive $500 of that credit, owe $0 in taxes, but forfeit the additional $500 credit value.

Common nonrefundable tax credits:

- Lifetime Learning Credit: A non-refundable credit worth up to $2,000 per return for higher education tuition and fees. There's no limit to the number of years you can claim it.

- Elderly or Disabled Credit: Gives taxpayers aged 65+ OR retired on permanent and total disability a nonrefundable credit ranging from $3,750 - $7,500.

These are just a few of the tax benefits you can take advantage of when you file your 2021 income tax returns. The IRS's Credits and Deductions for Individuals page provides a more comprehensive list of federal tax credits and deductions.

Legal Disclaimer - Please note, this material has been prepared for informational purposes only, and not intended to provide legal, tax, or accounting advice. Consultation with a legal, tax, or accounting advisor is advised.

You're about to exit BOH.com

Links to other sites are provided as a service to you by Bank of Hawaii. These other sites are neither owned nor maintained by Bank of Hawaii. Bank of Hawaii shall not be responsible for the content and/or accuracy of any information contained in these other sites or for the personal or credit card information you provide to these sites.