Economic & Market Monitor

For the period ending July 31, 2026

Market Review

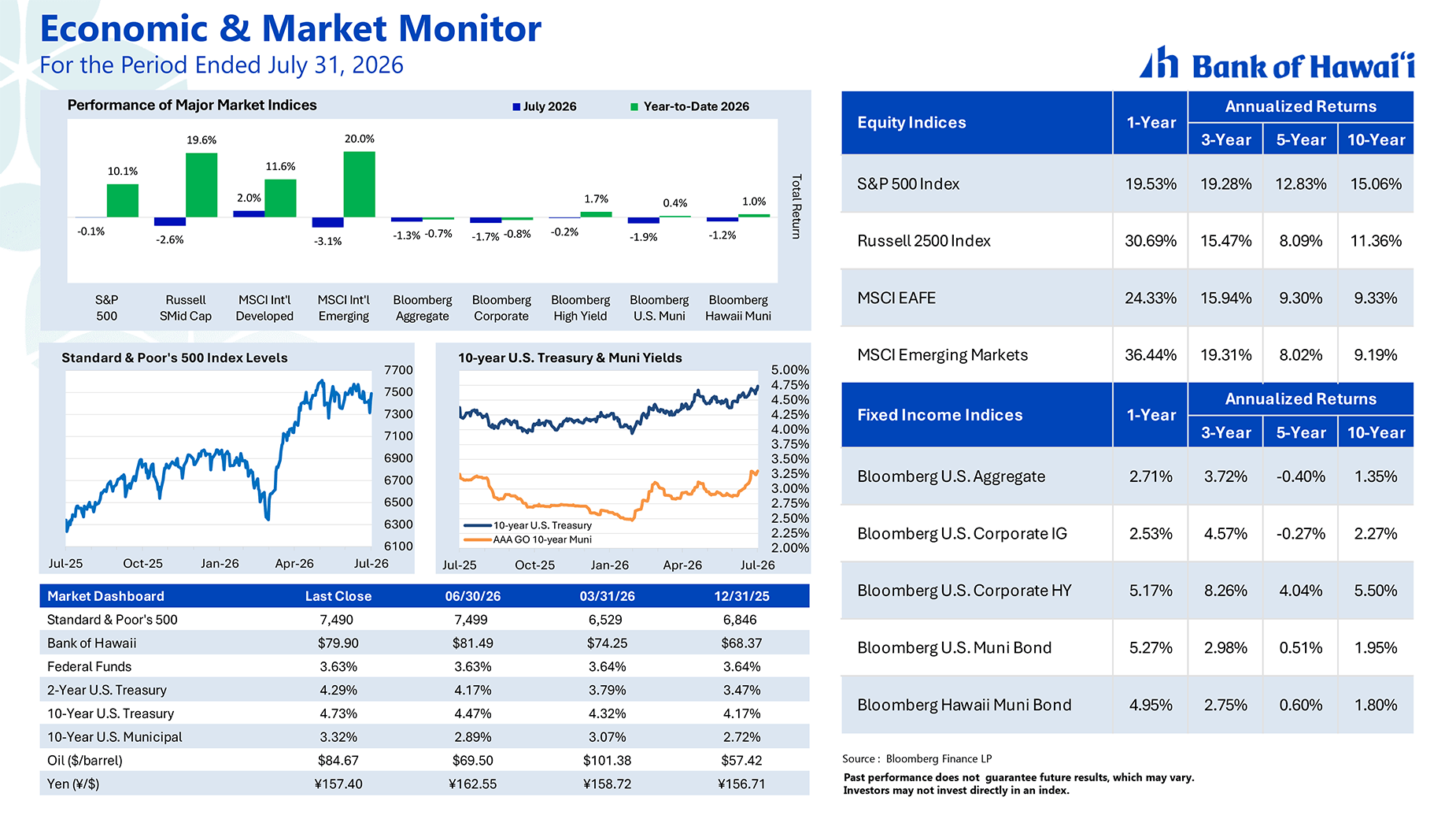

Profit Taking in Tech Stocks Drags on July Stock Market Returns: In a volatile month of trading, the S&P 500 Index slipped 0.1% in July, trimming its year-to-date return to 10.1%. The July decline was largely driven by weakness in the technology sector despite strong earnings results. The sector came under selling pressure as investors expressed concerns that heavy spending on artificial intelligence may not generate sufficient future profitability. S&P semiconductor stocks were particularly weak, falling 21.9% following their 94.4% surge during the first half of the year. Internationally, the MSCI EAFE Index (developed markets) gained 2.0%, while the MSCI Emerging Markets (EM) Index fell 3.1%. The performance differential was largely attributable to weakness in Taiwanese and South Korean semiconductor stocks held in the EM index. The year-to-date returns for these indexes were 11.6% and 20.0%, respectively.

Oil Prices Surge on Escalating Middle East Hostilities: Middle East tensions escalated sharply in July as the U.S. and Iran exchanged direct military strikes. Iran sought to exert control over the Strait of Hormuz, while Houthi forces threatened shipping in the Red Sea. The conflict expanded beyond Iran and Israel, with attacks targeting U.S. bases, regional infrastructure, and commercial maritime traffic, raising concerns about global energy supplies and trade routes. Oil prices, as measured by West Texas Intermediate futures, surged from $69.50 per barrel at the end of June to a high of $93.50 on July 23 before settling at $84.67 by month-end.

Higher Oil Prices Weigh on the Bond Market: Two-year and longer-term interest rates moved higher in July, largely in response to the rise in oil prices. The yield on 2-year U.S. Treasury notes increased from 4.17% to 4.29%, while the yield on 10-year U.S. Treasury notes rose from 4.47% to 4.73% during the month. Against this backdrop, the Bloomberg U.S. Aggregate Bond Index declined 1.3%, while the Bloomberg U.S. Municipal Bond Index fell 1.9%. Year-to-date returns for the two benchmarks were -0.7% and 0.4%, respectively.

Fed Holds Rates Steady While Signaling Higher Rates May Be Needed: At its July 29 Federal Open Market Committee (FOMC) meeting, members voted 9-3 to leave the federal funds target range unchanged at 3.50% to 3.75%. Although the decision itself was widely anticipated, the voting breakdown and accompanying commentary reflected a greater willingness to raise the federal funds rate in the future. The three dissenting FOMC members favored an immediate 0.25% rate increase. In its policy statement, the FOMC noted that economic activity continued to expand at a solid pace, supported by strong productivity gains, healthy business investment, and a labor market that remained resilient despite elevated uncertainty, including geopolitical tensions in the Middle East. At the same time, policymakers reiterated that inflation remains well above the Federal Reserve's 2% target, with higher energy costs and other supply-related pressures continuing to contribute to elevated price pressures. In June, the Fed's preferred inflation measure, the Core Personal Consumption Expenditures (PCE) Price Index, increased 3.3% year over year.

Federal Reserve Chairman Kevin Warsh reinforced that message during his post-meeting press conference, emphasizing the Fed's commitment to restoring price stability and noting that inflation has remained above the FOMC's 2% objective for more than five years. As of July 31, fed funds futures implied a 72% probability of a 0.25% increase in the federal funds rate at the FOMC's next scheduled meeting on September 16.

Inflation Remained Elevated but Eased in June: The Consumer Price Index (CPI) rose 3.5% year over year in June, down from 4.2% in May. Excluding food and energy prices, Core CPI eased to 2.6% from 2.9%. The Producer Price Index (PPI) increased 5.5%, down from 6.0% in May. However, Core PPI edged higher by 0.1 percentage point to 4.7%, though it remained below the Bloomberg consensus forecast of 5.1%.

Second-Quarter GDP Growth Moderated but Underlying Demand Remained Strong: The Bureau of Economic Analysis (BEA) reported that U.S. real gross domestic product (GDP) grew at an annualized rate of 1.5% during the second quarter. This was down from 2.1% in the first quarter and below the Bloomberg median forecast of 2.0%. The slower pace primarily reflected a decline in net exports and a drawdown in business inventories due to temporary factors. Importantly, the key drivers of economic growth remained strong despite uncertainty stemming from Middle East tensions. Consumer spending, which accounts for approximately two-thirds of U.S. economic activity, increased 3.2%, up from 0.5% in the first quarter. Business investment, fueled by continued AI-related spending, increased 8.4%. Although down from 10.6% in the first quarter, it remained well above its long-term growth rate of 4% to 5%.

Labor Market Holding Firm: The four-week moving average of initial unemployment claims for the week ended July 25 was 202,750, down from 219,250 at the beginning of the month. Meanwhile, continuing claims for unemployment benefits for the week ended July 18 totaled 1.782 million, down from 1.814 million at the end of June.

A Positive Reading on July Economic Activity: S&P Global's preliminary July Purchasing Managers' Index (PMI) registered 53.8, little changed from June's final reading of 53.9. PMI readings above 50 indicate expansionary economic conditions.

Second-Quarter Corporate Earnings Blow Past Forecasts: As of July 31, more than 60% of S&P 500 companies had reported second-quarter results, with 85% exceeding consensus earnings estimates. Analysts tracked by I/B/E/S estimate year-overyear second-quarter S&P 500 earnings per share (EPS) growth of 47.7%, nearly double the estimate at the start of the reporting period in early July. Full-year 2026 EPS growth is now projected at 30.8%, up from 26.6% a month ago.

Outlook

Possible Reprieve in Middle East Hostilities: The fundamental underpinnings of the stock market remain strong, but market direction in the coming weeks will be heavily influenced by developments in the Middle East. Positively, efforts to reach a diplomatic resolution appear to be gaining momentum. As of August 2, President Trump stated that planned U.S. strikes on Iran have been paused because a potential framework for a deal is emerging, and he expects U.S.-Iran negotiations to begin Monday. At the same time, Iranian and Omani officials report that discussions regarding the future reopening of the Strait of Hormuz are in their final stages, a key development for global energy markets. While President Trump's tone has shifted toward diplomacy, no agreement has been finalized, and conflicts in Gaza, Lebanon, and the Gulf continue to pose significant escalation risks.

Labor Market Reports: The Bureau of Labor Statistics will release July payroll, unemployment, and wage data on Friday. The median forecast of economists surveyed by Bloomberg calls for nonfarm payroll growth of 85,000, up from June's increase of 57,000. The unemployment rate and year-over-year wage growth are projected to remain unchanged at 4.2% and 3.5%, respectively.

Roger Khlopin, CFA

Chief Investment Officer

Aaron Nghiem, CFA, CIMA

Senior Portfolio Manager

This material is provided for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Bank of Hawaii and its affiliates do not provide tax, legal or accounting advice. This material is not intended to provide, and should not be relied on for, tax, legal, or investment advice. You should consult your own tax, legal, accounting or financial professional before engaging in any transaction. Neither the information nor any opinions expressed herein should be construed as a solicitation or a recommendation by Bank of Hawaii or its affiliates to buy or sell any securities, investments, or insurance products. Investing involves market risk, including possible loss of principal, and there is no guarantee that investment objectives will be achieved. Past performance is not a guarantee of future results.

You're about to exit BOH.com

Links to other sites are provided as a service to you by Bank of Hawaii. These other sites are neither owned nor maintained by Bank of Hawaii. Bank of Hawaii shall not be responsible for the content and/or accuracy of any information contained in these other sites or for the personal or credit card information you provide to these sites.